All Categories

Featured

Table of Contents

That commonly makes them a more cost effective choice for life insurance coverage. Many individuals get life insurance policy protection to aid financially secure their liked ones in case of their unanticipated fatality.

Or you may have the choice to transform your existing term protection into an irreversible policy that lasts the rest of your life. Different life insurance coverage plans have prospective benefits and disadvantages, so it's essential to recognize each prior to you decide to acquire a plan.

As long as you pay the costs, your beneficiaries will certainly receive the survivor benefit if you pass away while covered. That claimed, it is essential to note that most plans are contestable for 2 years which implies insurance coverage can be retracted on death, needs to a misstatement be located in the application. Policies that are not contestable usually have actually a graded survivor benefit.

Premiums are generally less than whole life plans. With a level term policy, you can pick your insurance coverage quantity and the plan size. You're not secured right into an agreement for the remainder of your life. Throughout your plan, you never have to bother with the costs or survivor benefit quantities transforming.

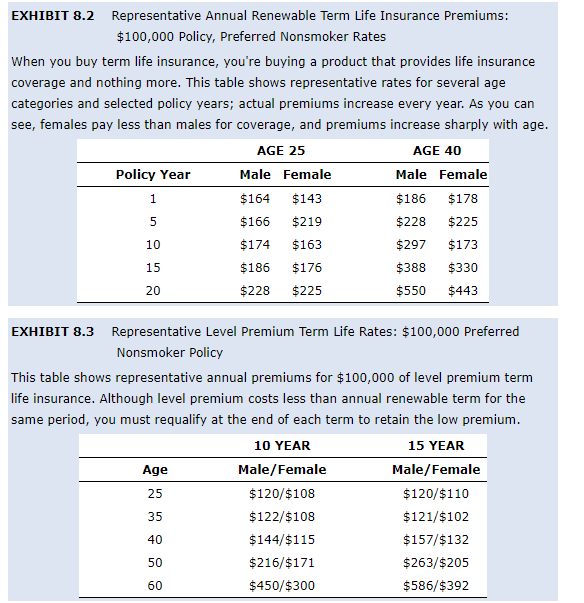

And you can't squander your plan throughout its term, so you won't receive any type of monetary gain from your past insurance coverage. Just like various other kinds of life insurance policy, the expense of a level term policy depends on your age, coverage demands, work, way of living and health. Usually, you'll discover a lot more budget-friendly coverage if you're younger, healthier and less dangerous to insure.

Innovative Increasing Term Life Insurance

Since degree term premiums stay the exact same for the period of insurance coverage, you'll recognize specifically just how much you'll pay each time. Degree term protection additionally has some versatility, permitting you to tailor your plan with added functions.

You might have to fulfill specific problems and credentials for your insurance provider to enact this motorcyclist. Furthermore, there might be a waiting duration of approximately 6 months prior to taking impact. There additionally might be an age or time limit on the coverage. You can add a child biker to your life insurance policy policy so it also covers your youngsters.

The death benefit is usually smaller sized, and protection usually lasts till your kid turns 18 or 25. This motorcyclist might be a much more cost-efficient means to assist guarantee your youngsters are covered as cyclists can often cover several dependents simultaneously. As soon as your kid ages out of this coverage, it may be possible to transform the cyclist right into a brand-new policy.

The most typical kind of long-term life insurance coverage is whole life insurance policy, yet it has some key differences contrasted to level term coverage. Here's a basic introduction of what to think about when contrasting term vs.

High-Quality The Combination Of Whole Life And Term Insurance Is Referred To As A Family Income Policy

Whole life entire lasts for life, while term coverage lasts protection a specific periodDetails The premiums for term life insurance policy are generally reduced than entire life insurance coverage.

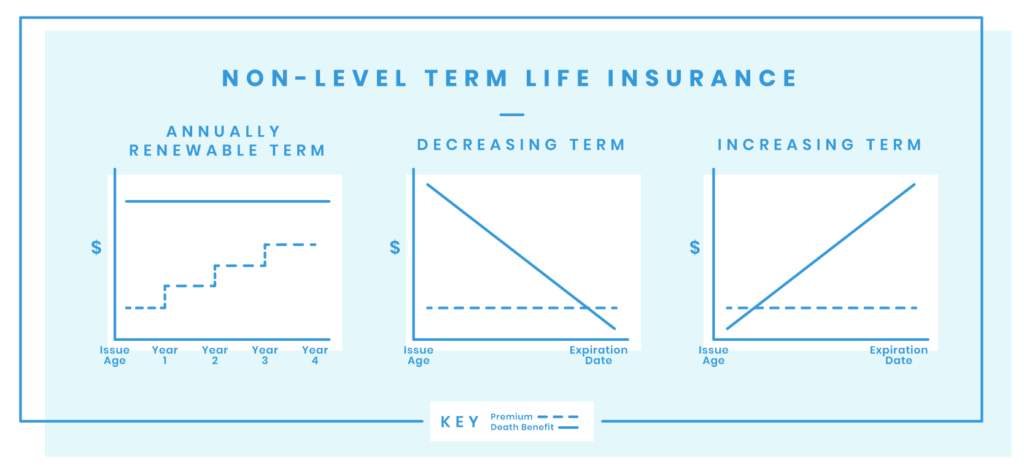

One of the main functions of degree term coverage is that your costs and your survivor benefit do not transform. With reducing term life insurance policy, your premiums remain the very same; however, the survivor benefit quantity gets smaller sized over time. You may have protection that starts with a death advantage of $10,000, which might cover a mortgage, and after that each year, the fatality advantage will certainly lower by a set quantity or percentage.

As a result of this, it's usually an extra budget-friendly kind of level term coverage. You might have life insurance policy with your employer, but it may not suffice life insurance policy for your needs. The very first step when buying a plan is figuring out just how much life insurance policy you need. Think about elements such as: Age Family members dimension and ages Work status Revenue Financial debt Way of life Expected final expenditures A life insurance policy calculator can help identify just how much you need to begin.

After choosing a plan, complete the application. For the underwriting process, you may need to provide basic individual, health and wellness, way of life and work information. Your insurance firm will identify if you are insurable and the risk you may offer to them, which is shown in your premium expenses. If you're accepted, sign the documentation and pay your first premium.

High-Quality Level Term Life Insurance

Finally, take into consideration scheduling time annually to review your plan. You might want to update your recipient details if you've had any substantial life modifications, such as a marital relationship, birth or divorce. Life insurance policy can often feel complicated. Yet you do not have to go it alone. As you explore your options, think about reviewing your requirements, desires and interests in an economic expert.

No, degree term life insurance policy doesn't have money value. Some life insurance coverage policies have a financial investment feature that allows you to build cash money value gradually. A portion of your premium payments is set apart and can gain passion over time, which grows tax-deferred during the life of your insurance coverage.

These plans are typically substantially much more expensive than term insurance coverage. If you get to the end of your policy and are still to life, the insurance coverage finishes. You have some choices if you still desire some life insurance coverage. You can: If you're 65 and your protection has gone out, as an example, you may want to buy a new 10-year degree term life insurance policy.

Affordable Annual Renewable Term Life Insurance

You might have the ability to transform your term coverage right into an entire life plan that will certainly last for the rest of your life. Lots of types of degree term policies are convertible. That suggests, at the end of your coverage, you can transform some or all of your policy to whole life coverage.

Degree term life insurance policy is a policy that lasts a set term usually between 10 and three decades and comes with a level fatality advantage and degree premiums that remain the same for the whole time the policy is in result. This implies you'll know precisely just how much your payments are and when you'll need to make them, permitting you to budget plan accordingly.

Level term can be an excellent choice if you're wanting to acquire life insurance coverage for the first time. According to LIMRA's 2023 Insurance policy Barometer Study, 30% of all adults in the U.S. requirement life insurance policy and don't have any type of kind of plan yet. Degree term life is predictable and affordable, which makes it one of one of the most prominent kinds of life insurance policy.

{kind=link}

Latest Posts

Funeral Policy For Over 80 Years

And Final Expenses

Funeral Plan Insurance Policies