All Categories

Featured

Table of Contents

It allows you to budget plan and plan for the future. You can easily factor your life insurance coverage right into your spending plan since the costs never change. You can prepare for the future just as easily due to the fact that you recognize precisely just how much cash your loved ones will receive in case of your lack.

In these instances, you'll usually have to go with a new application procedure to get a much better price. If you still require coverage by the time your degree term life plan nears the expiry date, you have a couple of options.

The majority of level term life insurance policy policies include the option to renew protection on an annual basis after the initial term ends. joint term life insurance. The expense of your plan will be based upon your existing age and it'll raise annually. This could be a good option if you just need to extend your protection for one or two years otherwise, it can get pricey rather quickly

Degree term life insurance coverage is among the least expensive insurance coverage choices on the market due to the fact that it offers basic protection in the type of death benefit and only lasts for a set amount of time. At the end of the term, it runs out. Entire life insurance policy, on the other hand, is significantly a lot more costly than level term life due to the fact that it doesn't end and comes with a money value function.

Guaranteed Issue Term Life Insurance

Prices may vary by insurance company, term, insurance coverage amount, health and wellness class, and state. Level term is an excellent life insurance option for the majority of individuals, but depending on your insurance coverage needs and individual situation, it might not be the ideal fit for you.

Yearly sustainable term life insurance policy has a term of just one year and can be renewed every year. Annual sustainable term life premiums are originally lower than degree term life premiums, but costs increase each time you renew. This can be a great option if you, for instance, have just give up smoking cigarettes and need to wait two or three years to look for a level term policy and be eligible for a lower rate.

Innovative Level Term Life Insurance Meaning

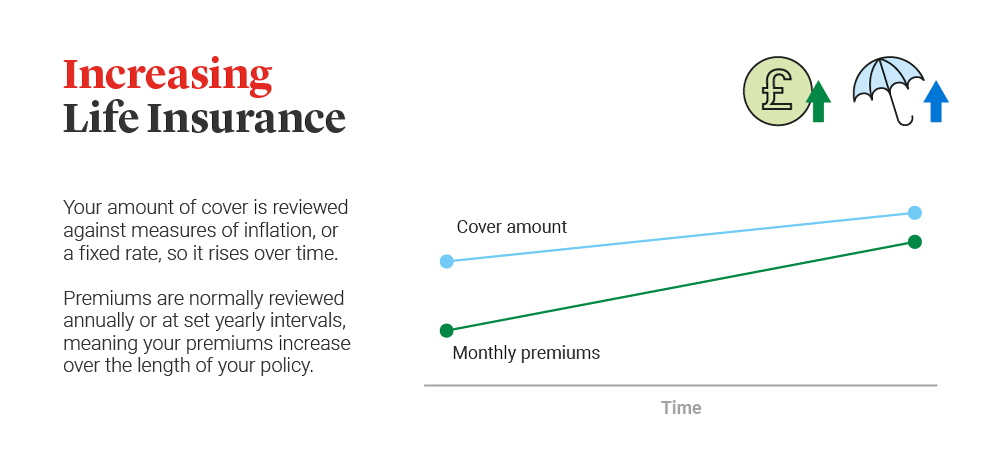

, your death advantage payout will certainly lower over time, yet your settlements will certainly stay the same. On the other hand, you'll pay even more ahead of time for less coverage with a boosting term life policy than with a level term life plan. If you're not certain which type of policy is best for you, working with an independent broker can help.

Once you have actually made a decision that level term is right for you, the following action is to buy your policy. Here's how to do it. Calculate how much life insurance you require Your coverage amount should offer your family's long-term monetary requirements, including the loss of your income in case of your fatality, along with financial obligations and daily expenditures.

A level costs term life insurance coverage strategy allows you stick to your budget plan while you help secure your household. ___ Aon Insurance Providers is the brand name for the brokerage and program administration operations of Fondness Insurance policy Providers, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Affinity Insurance Coverage Company, Inc. (CA 0795465); in Alright, AIS Affinity Insurance Policy Solutions Inc.; in CA, Aon Affinity Insurance Coverage Providers, Inc.

The Plan Agent of the AICPA Insurance Coverage Depend On, Aon Insurance Policy Services, is not affiliated with Prudential.

{kind=link}

Latest Posts

Buying Mortgage Insurance

Cost-Effective Voluntary Term Life Insurance

Leading Term Life Insurance With Accelerated Death Benefit